Price Discipline Isn't The Same As Price Anxiety

In a general partner group chat recently, someone shared the "crazy" news about a YC company with a $50M cap closing $5M in 4 days. Two "mind blown" emoji reactions in shared disbelief, and a lot of silence.

The reactions, or lack thereof, reflect two distinct perspectives on pricing: those who won't invest above a certain valuation, and others who believe price doesn't matter as long as the company is great. While understandable, both viewpoints are reactions to a number rather than a framework for considering it. Venture has always had more gut feel than institutional rigor, more hand-waving than hard analysis. We should push back on that, and pricing decisions are a good place to start.

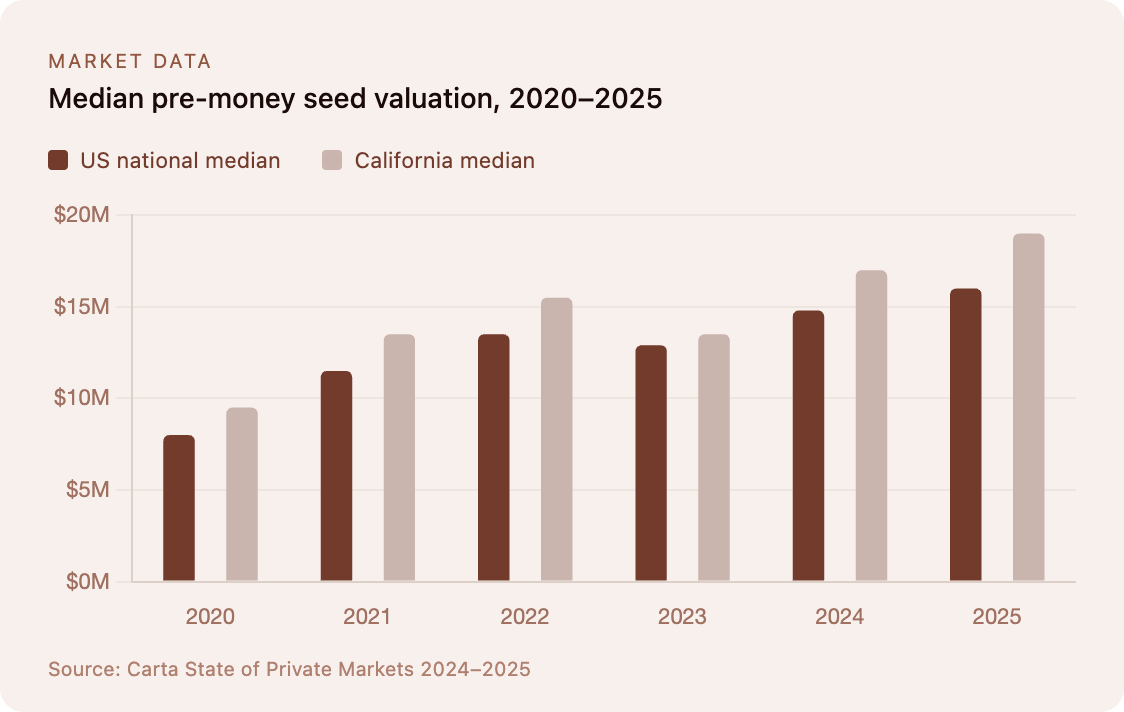

The data is real

The YC company in the group chat reflects real market movement. According to Carta data through Q1 2026, the national median post-money seed valuation is $24M—but the headline number undersells what's actually happening. The 95th percentile has hit $173.6M, up from $65.6M just four years ago. The 90th percentile is $93.7M. The 75th percentile is $44M. And the 25th percentile is $22.7M. The market hasn't just bifurcated—the top of it has gone parabolic, while the broad middle has barely moved. That gap is the story.

Price is the wrong starting point

Price anxiety is a reaction to a number. Price discipline is something else. It starts with the fund model, derives required ownership, and only then asks whether a given entry price is consistent with generating a return.

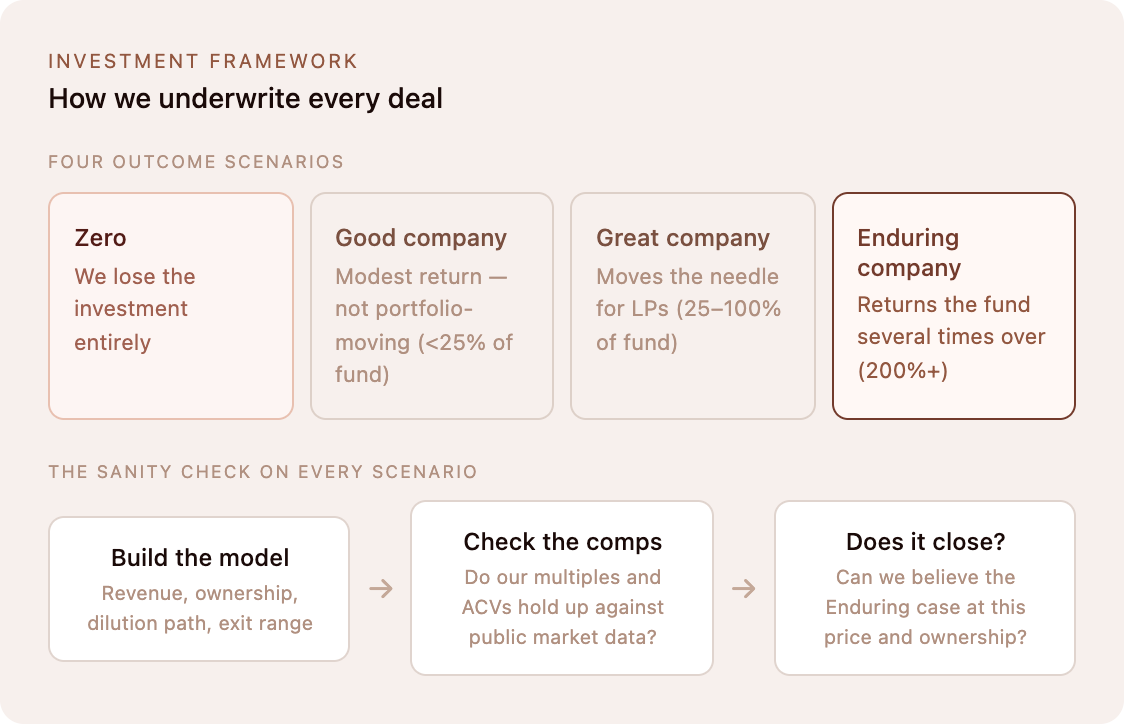

At Penny Jar, we are underwriting $10B in enterprise value across our portfolio in our current fund to deliver a 5x net return. That North Star determines the weighted average ownership we need. Price matters to the extent it determines ownership, and ownership determines whether our winners can actually move the fund.

For every potential investment, we build out four scenarios:

- Zero — we lose everything

- Good Company — modest return for the fund, but doesn't move the needle for our LPs (returns <25% of fund)

- Great Company — good return for the fund, moves the needle for our LPs (25–100% of fund)

- Enduring Company — returns the fund several times by itself (200%+ of fund)

We model each, then anchor the assumptions to public-market comparables. If our best case requires $5M annual contract values but the category incumbent is doing $500K, that gap needs hard evidence, not optimism. A price that only makes sense if unanchored assumptions hold isn't price discipline — it's hope.

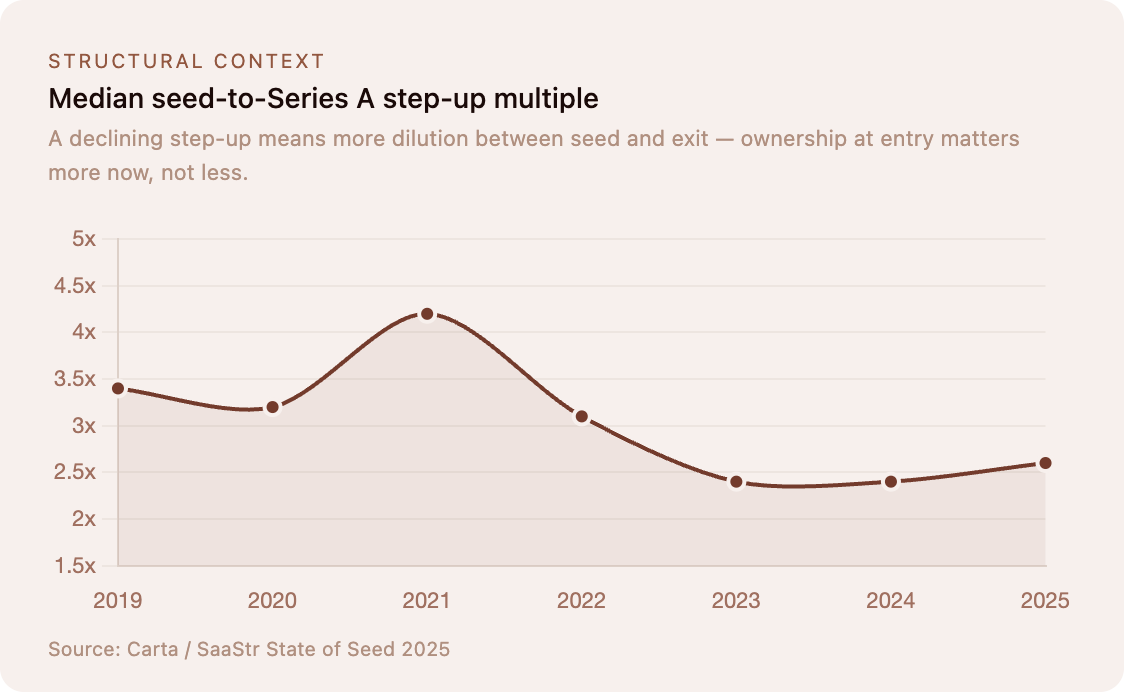

The step-up multiple from seed to Series A has also declined, from a peak of 4.2x in 2021 to 2.6x today. That structural compression means ownership at entry matters more now, not less.

Exceptions are fine. Drift is not.

Our best-performing investments prove the point in reverse: when a company is on its way to market leadership, the entry price gets swamped by the result. Excessive price discipline would've cost us those positions, so we make exceptions.

But if most of our investments require exception-level justification, we no longer have a strategy. We distinguish an exception from drift by staying tethered to the fund model logic. Is there still a credible path to meaningful returns in the Great Company and Enduring Company scenarios? If yes, the exception is defensible. If, instead, we're tethered to hope, it's not an exception. It's just paying too much.

A Framework, Not a Feeling.

Seed prices are going up. That's the reality, and a hard cap will naturally miss some of the very best founders who are justifiably commanding higher prices. An investment strategy based on an arbitrary line in the sand isn't discipline; it's more like putting on blinders.

Better to consider pricing within a framework, rather than reacting with a feeling. Know what the market is paying. Build the scenario math. Check it against comps. And evaluate each deal to determine whether the ownership at the price can close the return to fund-meaningful levels.

That's the difference between price discipline and price anxiety. One is a process. The other is a reaction. Only one of them belongs in an investment memo.

Up next

The female founders shaping Israel’s startup scene in 2025

The Founder Apple Let Get Away